Florida, Homeowners Insurance, Hurricane Claims, Property Insurance Claims

Florida Homeowners Insurance Reviews: What Homeowners Need to Know Before Choosing Coverage

Florida homeowners face some of the highest insurance costs and most complex property insurance challenges in the country. Between hurricanes, severe storms, rising premiums, and policy restrictions, many homeowners are searching for reliable information about homeowners insurance reviews, policy options, and what coverage may actually protect their property.

Understanding how homeowners insurance works in Florida can help homeowners make more informed decisions before disaster strikes.

Why Florida Homeowners Insurance Has Become More Complicated

Florida’s insurance market has changed significantly in recent years due to:

- Increased hurricane and storm activity

- Rising construction and repair costs

- Insurance carrier insolvencies

- Higher claim payouts

- Increased litigation involving property claims

As a result, many homeowners are seeing:

- Higher premiums

- Larger deductibles

- Reduced coverage options

- More policy exclusions

- Stricter underwriting requirements

Homeowners comparing insurance companies often look beyond pricing alone and focus on reviews involving claim handling, customer service, and payout reliability.

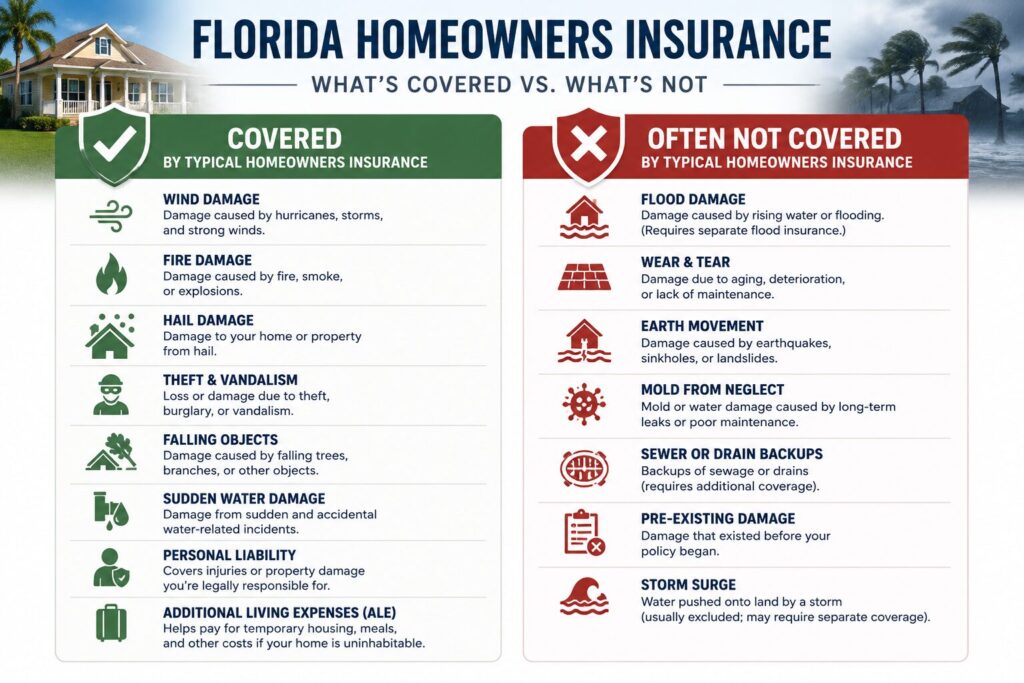

What Homeowners Insurance Typically Covers

Most standard homeowners insurance policies may provide protection for:

Dwelling Coverage

Coverage for damage to the home itself, including:

- Roof damage

- Structural damage

- Wind damage

- Fire damage

- Lightning strikes

- Certain water-related losses

Personal Property Coverage

Coverage for belongings inside the home, including:

- Furniture

- Electronics

- Clothing

- Appliances

Additional Living Expenses

If a home becomes uninhabitable after covered damage, policies may help cover:

- Hotel stays

- Temporary housing

- Food expenses

- Other necessary living costs

Liability Protection

Coverage may also help protect homeowners if someone is injured on the property.

To better understand policy protections, read:

What Does Homeowners Insurance Cover?

What Florida Homeowners Should Watch for in Insurance Reviews

When reviewing homeowners insurance companies, homeowners should look closely at more than monthly premium costs.

Important review factors may include:

Claim Response Time

How quickly does the insurer respond after a claim is filed?

Hurricane Claim Handling

How does the company handle hurricane-related damage claims?

Underpaid Claim Complaints

Are policyholders reporting low settlement offers?

Denied Claim Patterns

Does the company have a history of disputed or denied claims?

Customer Service Reputation

Can homeowners easily reach adjusters and claim representatives?

Why Hurricane Coverage Matters in Florida

Florida homeowners are especially vulnerable to:

- Hurricane wind damage

- Roof damage

- Water intrusion

- Storm surge flooding

- Mold and moisture issues

Many homeowners mistakenly believe all hurricane-related damage is automatically covered. However, policies often contain:

- Hurricane deductibles

- Windstorm exclusions

- Coverage limitations

- Flood exclusions

To learn more about documenting losses after severe weather, review:

How to Document Storm Damage for Your Insurance Claim

Common Reasons Florida Insurance Claims Are Underpaid

Some homeowners receive settlement offers that do not fully cover repair costs. Common disputes may involve:

- Roof replacement scope disagreements

- Depreciation calculations

- Delayed inspections

- Hidden damage disputes

- Partial payment offers

- Questions about pre-existing damage

If your claim settlement seems too low, review:

How to Fight an Underpaid Insurance Claim

How to Compare Florida Home Insurance Policies

When comparing homeowners insurance policies, homeowners should review:

Deductibles

Understand both standard deductibles and hurricane deductibles.

Coverage Limits

Make sure limits reflect realistic rebuilding costs.

Exclusions

Carefully review exclusions involving:

- Flooding

- Roof age

- Mold

- Water damage

- Windstorm limitations

Claim Process

Research how the company handles large-scale storm claims.

Steps Homeowners Should Take Before Hurricane Season

Preparing before a storm may help strengthen a future insurance claim.

Homeowners should:

- Review their current insurance policy

- Photograph the property before storm season

- Maintain copies of important documents

- Create a home inventory

- Understand deductible requirements

- Inspect roofs and vulnerable areas regularly

What to Do After Property Damage

After storm or hurricane damage:

- Document all visible damage immediately

- Take photos and videos before cleanup

- Save receipts for emergency repairs

- Keep records of all insurer communications

- Avoid accepting low settlements too quickly

How Morgan Law Group Helps Homeowners

Insurance disputes can become overwhelming when homeowners are dealing with denied, delayed, or underpaid property claims. Morgan Law Group helps policyholders pursue compensation involving:

- Hurricane damage claims

- Roof damage claims

- Windstorm losses

- Water intrusion claims

- Underpaid insurance claims

- Delayed claim investigations

Get Help With a Bad Faith Insurance Claim

If your hurricane claim was delayed, denied, or underpaid unfairly, we can help you take the next step.

Frequently Asked Questions

Why are Florida homeowners insurance rates increasing?

Florida insurance premiums have increased due to hurricane risks, rising repair costs, insurer losses, and increased claim payouts across the state.

Does homeowners insurance cover hurricane damage?

Many policies cover hurricane wind damage, but flood damage is usually excluded unless separate flood insurance coverage exists.

What should I look for in homeowners insurance reviews?

Homeowners should evaluate claim handling, customer service, payout disputes, deductible structures, and policy exclusions when comparing insurance companies.

What should I do if my insurance claim is underpaid?

You should document all damages, review your policy carefully, gather repair estimates, and consider speaking with a property insurance attorney if the settlement does not fully cover your losses.